You've been binge-watching flipping shows, running numbers on Zillow at midnight, and driving through Phoenix neighborhoods looking for "the one." You're ready to do your first fix-and-flip. There's just one problem: you have no idea how to actually pay for it.

If you've looked into financing, you've probably heard the term "hard money loan" and wondered if it's something you should be excited about or terrified of. The name doesn't exactly sound friendly. And when you start Googling, you find interest rates that seem high, terms you don't fully understand, and a nagging fear that you won't qualify because you've never done this before.

Here's the good news: hard money loans are actually the most beginner-friendly way to finance a fix-and-flip. And by the time you finish reading this guide, you'll know exactly how they work, what you need to qualify, what they actually cost, and how to avoid the mistakes that trip up first-time investors.

What Is a Hard Money Loan? (The Plain-English Version)

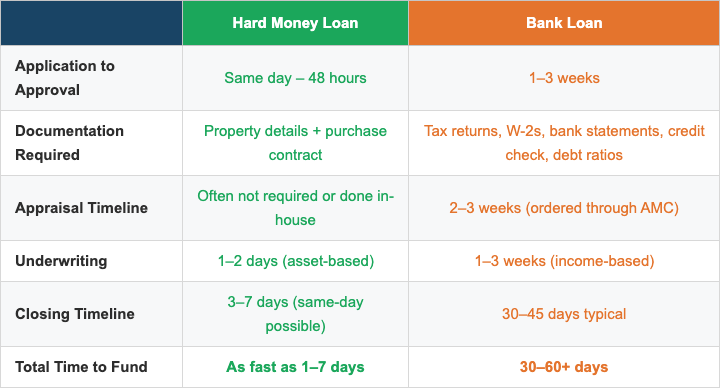

A hard money loan is a short-term loan used to buy and renovate investment properties. Unlike a bank loan, which is based on your income, credit score, and financial history, a hard money loan is based primarily on the property itself — what it's worth now and what it will be worth after you fix it up.

That second number — the after-repair value, or ARV — is what matters most. If the deal makes sense on paper (buy it cheap, rehab it, sell it for a profit), a hard money lender will fund it. They're not as concerned about your W-2 or your credit score. They're looking at the asset.

Hard money loans are typically 6 to 18 months, which is perfect for a flip timeline. You borrow the money, do the renovation, sell the property, and pay back the loan. The whole cycle might take 4 to 7 months.

Do I Qualify? What Hard Money Lenders Actually Look For

This is the question that keeps first-time flippers up at night. The answer is probably going to surprise you: qualifying for a hard money loan is much easier than qualifying for a bank loan.

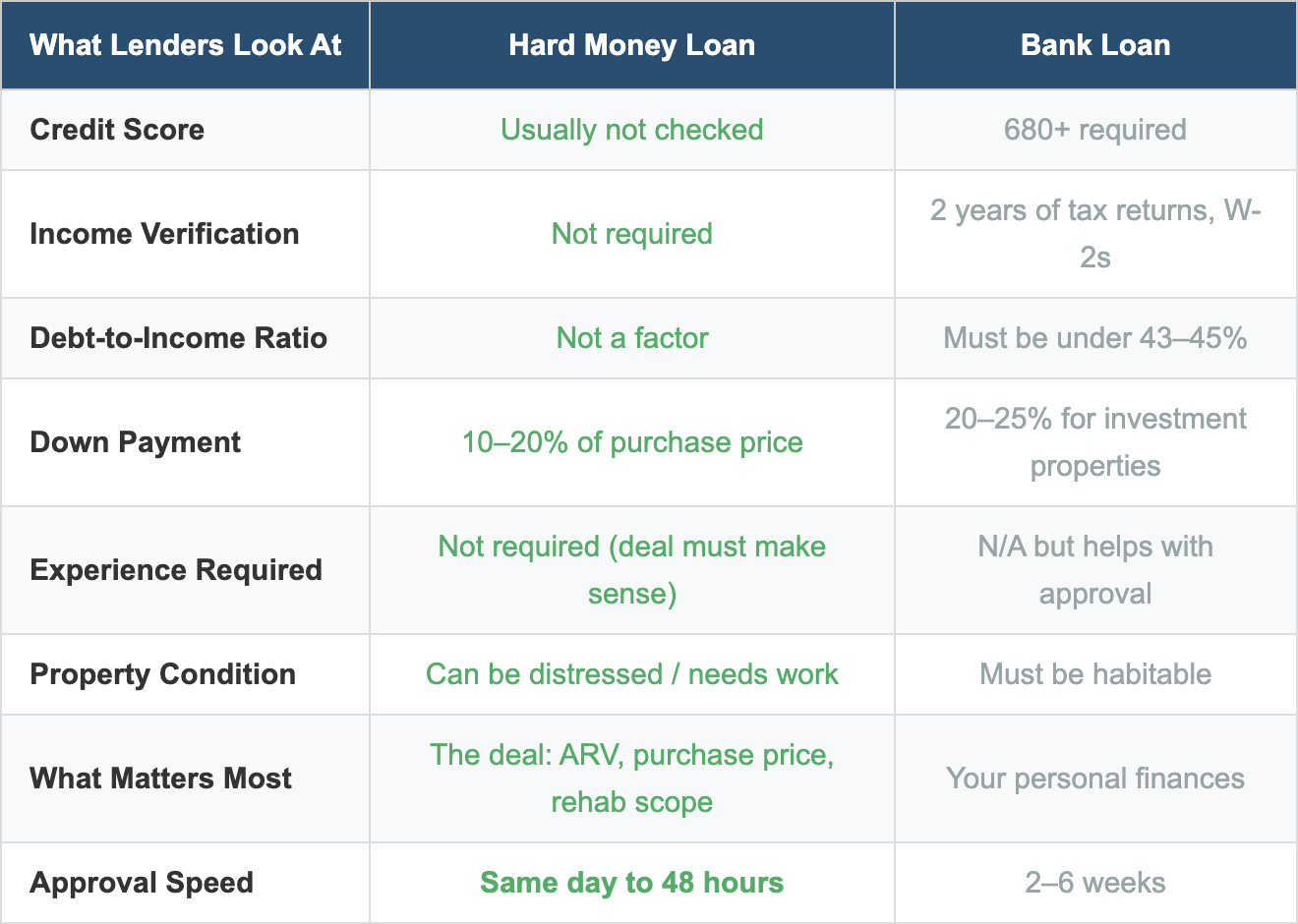

Here's what most hard money lenders evaluate:

See the pattern? With a hard money loan, the property qualifies you, not your personal financial history. That's why hard money is the go-to financing for first-time flippers — you don't need years of experience or a perfect credit score. You need a solid deal.

What Does a Hard Money Loan Actually Cost?

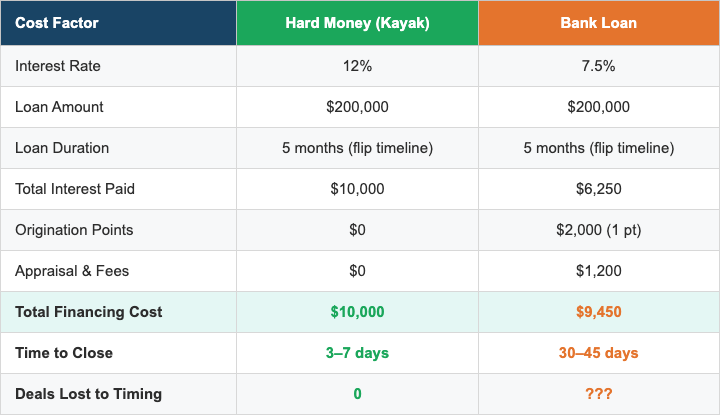

Let's talk dollars, because this is where a lot of beginners get confused — or scared off. Hard money interest rates are higher than bank rates, typically 9–12%. But remember, you're only paying that rate for a few months, not 30 years. The total interest on a short-term flip is usually very manageable.

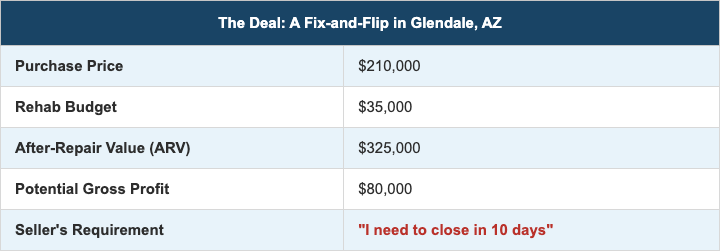

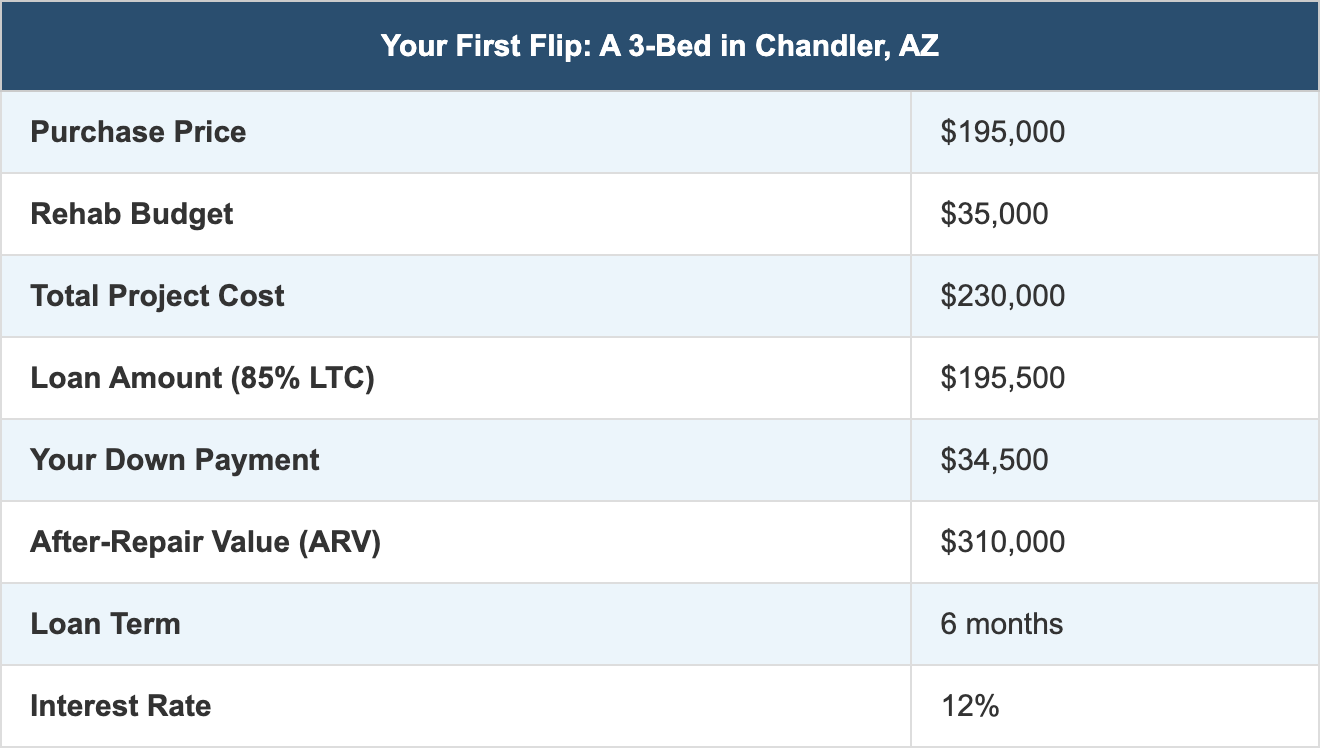

Here's what a realistic first flip might look like in the Phoenix metro:

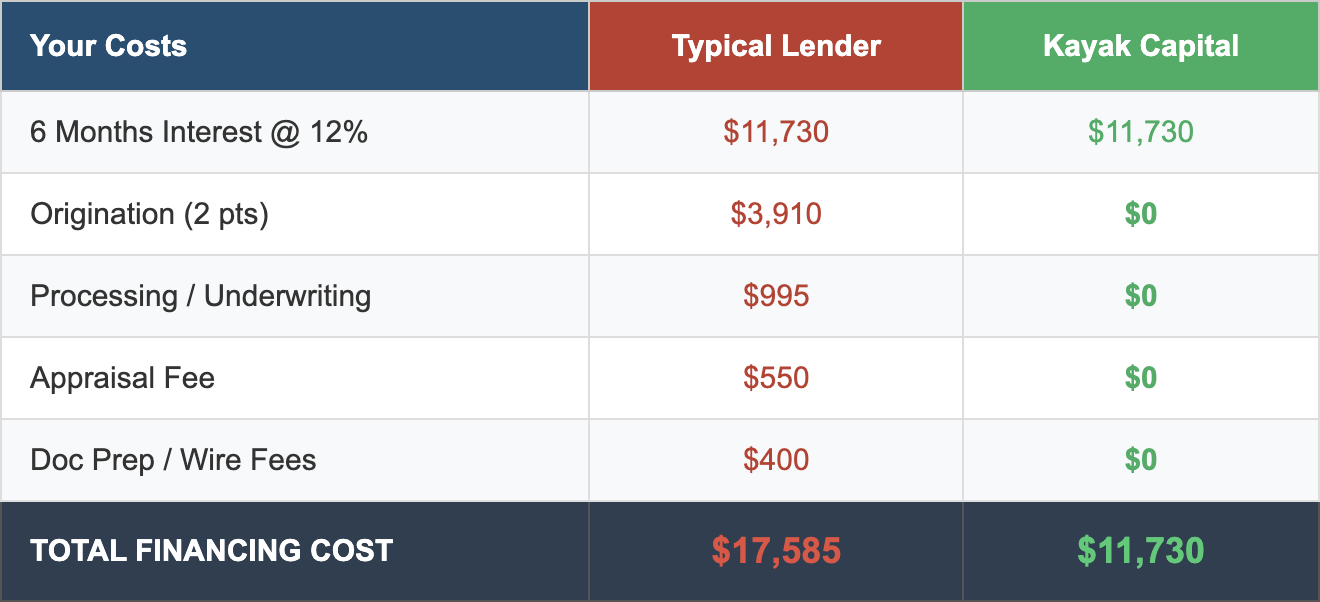

With Kayak Capital, you save $5,855 on your very first deal. That's money that stays in your pocket to fund the next one. And since your total project cost is $230,000 and the ARV is $310,000, your gross profit on this flip would be roughly $80,000 before financing costs — minus $11,730 in interest with Kayak, leaving you with a healthy return even on deal number one.

The 5 Steps to Getting Your First Hard Money Loan

The process is simpler than you think. Here's how it works, step by step:

Step 1: Find Your Deal. Before you talk to a lender, find a property that makes sense on paper. Run the numbers: purchase price + rehab cost should leave you with at least 20–25% profit margin after all costs. Use the 70% rule as a quick gut check — your total investment (purchase + rehab) should be no more than 70% of the ARV.

Step 2: Call Your Lender. With Kayak Capital, you call (480) 256-2274 or fill out the online application (takes under 3 minutes). Share the property address, purchase price, estimated rehab budget, and your projected ARV. That's it — no tax returns, no credit pull, no 47-page application.

Step 3: Get Approved. Kayak Capital approves loans within 1 hour. We'll review the deal, confirm the numbers make sense, and give you a clear answer fast. No waiting days or weeks wondering if you're approved.

Step 4: Close the Deal. Once approved, we coordinate with your title company to get the file completed. You sign docs at the title company on closing day and funds are wired the same day. The entire process from approval to funding can happen in as little as a few days.

Step 5: Renovate, Sell, Repeat. Do the rehab, list the property, sell it, and pay off the loan. With Kayak Capital, there's no prepayment penalty and no minimum interest requirement — you only pay interest for the days you actually use the loan. The faster you flip, the less you pay.

5 Mistakes First-Time Flippers Make (And How to Avoid Them)

1. Underestimating rehab costs. Always add a 10–15% buffer to your contractor's bid. Surprises are the rule, not the exception — especially with older Phoenix homes where you might find outdated plumbing, asbestos, or unpermitted work behind the walls.

2. Ignoring carrying costs. Interest, insurance, property taxes, utilities, and HOA dues (if applicable) all add up while you're holding the property. On a $200,000 loan at 12%, you're paying roughly $2,000/month in interest alone. Factor this into your profit calculation from day one.

3. Over-improving for the neighborhood. Don't put $80,000 in finishes into a $300,000 neighborhood. Your comps set the ceiling. Study what recently sold homes in the area look like and match that level — don't exceed it.

4. Not having an exit strategy. Before you close, know exactly how you're going to sell the property. What's the target list price? What's the market doing in that neighborhood? How long are comparable homes taking to sell? Your lender will ask about your exit plan, and you should have a clear answer.

5. Choosing a lender based on rate alone. A lender with a 10% rate but $6,000 in fees costs you more than a lender with a 12% rate and zero fees. Always compare total cost of financing, not just the interest rate. And factor in how fast they can close — because a slow lender can cost you the deal entirely.

Why Kayak Capital Is Built for First-Time Flippers

A lot of hard money lenders say they work with beginners. But when you actually apply, you find out they want two years of experience, a 650+ credit score, and $5,000–$8,000 in upfront fees. That's not exactly beginner-friendly.

Here's what makes Kayak Capital different:

- No experience required. If the deal makes sense, we fund it. We've worked with hundreds of first-time investors over nearly 15 years.

- No credit pull. We don't check your credit score. The property is the collateral, not your FICO.

- Zero fees. No origination points, no processing fees, no appraisal fees, no junk charges. The interest rate is your only cost.

- Fast and simple. Apply in under 3 minutes. Get approved in 1 hour. Close as fast as title can prep the docs.

- Direct decision-makers. When you call Kayak Capital, you talk to the people who make the lending decisions — not a call center, not a loan officer who has to "run it up the chain." We lend our own money, so we decide fast.

We've funded over 1,700 deals across the Phoenix metro area. Many of those started with someone just like you — a first-time flipper with a solid deal and the motivation to make it happen.

Ready to Fund Your First Flip?

Your first deal is the hardest — not because the process is complicated, but because everything is new. The right lending partner makes all the difference. At Kayak Capital, we make it simple: no fees, no hassle, and a real person on the other end of the phone who wants to see you succeed.

Here's how to get started:

- Call us at (480) 256-2274 — talk directly to a decision-maker, not a call center.

- Apply online in under 3 minutes at KayakCapital.com.

- Get approved within 1 hour and close as fast as your title company can get the docs ready.

Zero points. Zero fees. Your only cost is the interest rate. Let's get your first flip funded.

Related Reading

Hard Money Loan Fees Are Killing Your Flip Profits — Here's the Math